The National Assembly of the Republika Srpska adopted the Annual Audit Report for 2023 at its fifth regular session, and took note of the Report on the financial audit of the Consolidated Annual Financial Report for the budget users of the Republika Srpska for the period from January 1 to December 31, 2022.

The Supreme Audit Office of the Republic of Srpska public sector submitted to the National Assembly of the Republic of Srpska together with the report on the audit of the Consolidated Annual Financial Report for the users of the budget of the Republic of Srpska and the Annual Audit Report for 2023, which includes the most important findings and recommendations from the financial audit and performance audit for the past reporting period, from September 1, 2022, to July 31, 2023.

In accordance with the plans of audit activities for 2022 and 2023, 71 financial audits were carried out in the indicated reporting period, which includes the audit of financial statements and, together with it, the audit of compliance, namely audits:

- 21 beneficiaries of the budget of the Republic of Srpska where a financial audit is mandatory every year according to the Law on Auditing the Public Sector of the Republic of Srpska,

- four social funds,

- Consolidated annual financial report for the beneficiaries of the revenue of the budget of the Republic of Srpska for the year 2022,

- 16 municipalities

- 17 entities in the field of health care (hospitals, health centers, and institutes);

- eight faculties;

- three other entities of the republic administration and one joint stock company.

Based on the conducted financial audits for the previously mentioned entities, the following opinions were given:

– opinion on financial statements:

- unqualified opinion for 29 subjects;

- qualified opinion for 36 reports and

- six adverse opinions.

– opinion on compliаnce:

- unqualified for 21 subjects;

- qualified opinion for 46 reports and

- four adverse opinions.

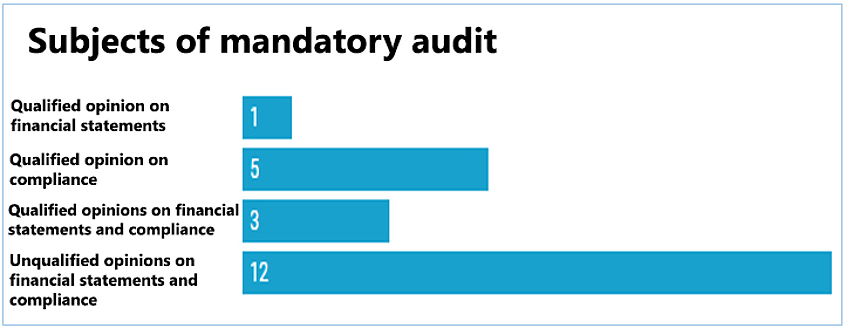

Of the 21 entities where the financial audit is mandatory every year, unqualified opinions (both for financial statements and for compliance) were expressed for 12 of them, while qualified opinions were expressed for the other entities, thereby for three entities qualified opinions were expressed for financial statements as well as compliance, five ministries have a qualified opinion on compliance (with a unqualified opinion on FS), and one ministry has a qualified opinion on financial statements. In addition, both opinions are qualified for the Consolidated Annual Financial Report of the beneficiaries of the Republic’s budget for the year 2022.

Implementation of recommendations from the financial audit report for the previous year

Considering that the financial audit of these entities is carried out every year, the status of previously given recommendations is checked and this is stated in a separate chapter of each audit report. Certain entities consistently implement audit recommendations, while the same or similar recommendations are repeated in the case of a part of budget users, that is, no activities have been undertaken to eliminate the identified non-compliances.

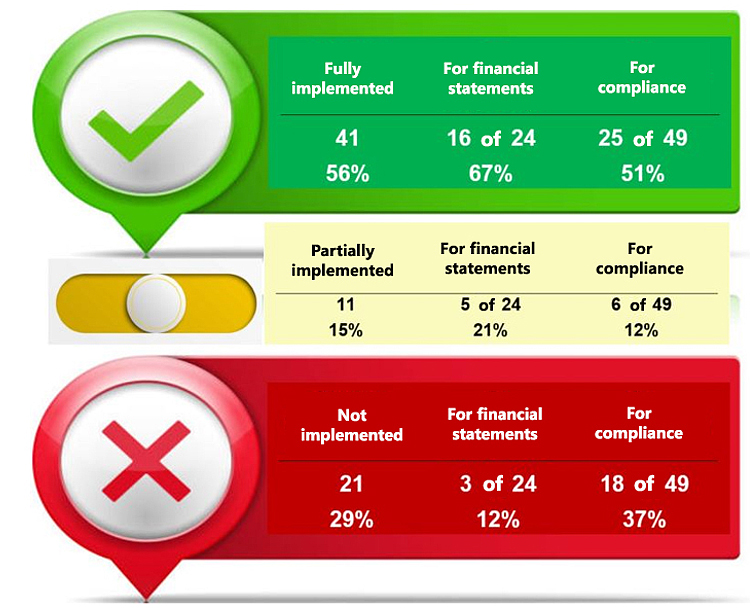

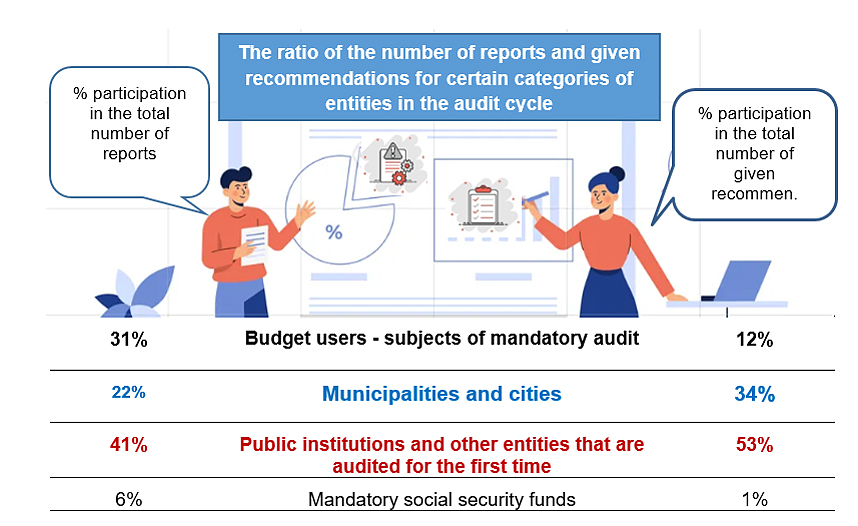

Although almost every third financial audit report in this audit cycle refers to subjects of mandatory audit (budgetary users and funds defined by the Law), the smallest number of recommendations (an average of 3.5 per report) were addressed to these subjects, with the largest percentage of participation positive opinions (over 70%).

On the other hand, audit subjects that are not audited in regular annual cycles, and in this case they were mainly public institutions (health centers, hospitals, faculties, institutes and other entities) that were not subject to public sector audits, were given more than half of all recommendations, a total of 367, i.e. 189 for financial statements and 178 for compliance. The fact that an average of 13 recommendations per report were given to these entities points to the conclusion that in connection with these audits, it will be necessary to carry out at least one more engagement to check the status of the given recommendations.

In addition, more than a third of all given recommendations, more precisely 244 recommendations, were sent to municipalities in this reporting period (through 16 financial audit reports, including 8 audits in the period from September 1 to December 31, 2022 and 8 that were carried out in 2023.). The complexity of the financial audit of municipalities (consolidated FR that includes lower budget users; conducting audits every 3-4 years) is clearly reflected in the scope of identified deficiencies, but also in the number and structure of recommendations. An average of 15 recommendations per report indicates that it is necessary to strengthen and improve the system of financial reporting and internal financial control in municipalities/cities, as well as the mechanisms and modalities of parliamentary supervision.

Performance audit

In the indicated reporting period, six performance audits were conducted through which the Supreme Audit Office offered a total of 41 recommendations to the Government of the Republic of Srpska, ministries, public enterprises, public institutions, municipalities and other public sector institutions that are competent and responsible for managing processes and activities who were subject to a performance audit. The institutions included in the audit, in accordance with the Law, expressed their views on the draft performance audit reports in the form of comments, and very affirmatively on the topics and reports of the performance audit.

By choosing the areas of audit and topics that are the subject of the performance audit, the Supreme Audit Office is in the function of achieving the general goals established by the strategies and policies of the Republic of Srpska and the function of improving general and financial management in the public sector of the Republic of Srpska. In order to fulfill the general objective of the performance audit, the audit process includes several public sector institutions that have certain roles, responsibilities, and responsibilities related to the processes and activities that are the subject of the audit for a long period.

A number of performance audit engagements relate to the topic of sustainable development and serve the purpose of implementing the Agenda 2030 Sustainable Development Goals in the Republic of Srpska.

Implementation of performance audit recommendations

The public registry of performance audit recommendations was established in 2014, and was redesigned in 2020 and represents a more meaningful information base for all interested users. The establishment of the register of recommendations aims to present in a unique and systematic way the recommendations that the Supreme Audit Office gives to public sector institutions in performance audit reports.

The joint activities of the institutions included in the audit, the Audit Committee of the National Assembly of Republika Srpska and the Supreme Audit Office increased the number and quality of action plans for the implementation of performance audit recommendations, compared to previous audit cycles. The very fact that the number of submitted action plans is greater than the number of institutions included in the audit shows that the institutions that were not included in the audit recognized the importance of the recommendations of the performance audit and the need to implement them in order to improve the processes and activities within their jurisdiction.

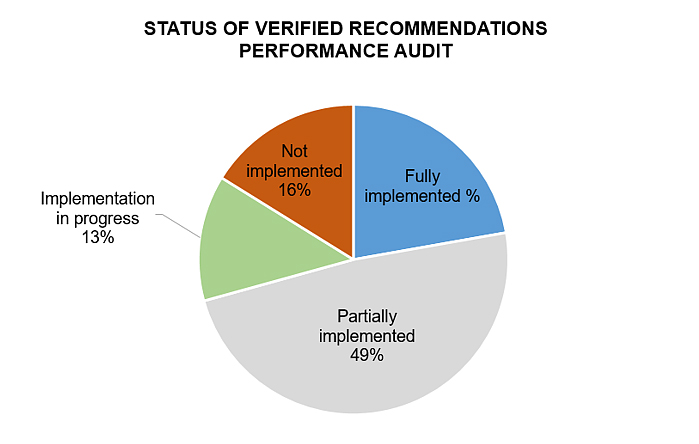

In accordance with the annual audit plans, in the previous period, including this audit cycle, 16 follow-up engagements were conducted and 116 performance audit recommendations were verified.

The Annual plan of audits for 2023 foresees the implementation of 86 audits of financial statements and compliance audits, six performance audits, four subsequent follow-up reviews of the implementation of performance audit recommendations from previous years and the maximum possible number of engagements to check status of recommendations from financial audit reports.